As a $5-trillion global business, the chemical industry has grown significantly during the last 50 years. The chemical business consumes 26 percent of its own output, making it one of the largest consumers in this space. Other top chemical consuming industries include agriculture, automotive and the construction business. The chemical industry is concentrated in three major regions—North America, Western Europe and China—and the outlook in each region is expected to vary.

North America

The U.S. is responsible for 15 percent of the global chemical output, with more than 170 companies operating internationally. The shale oil and gas boom’s impact for U.S. chemical companies has resulted in a decrease in the costs of energy and raw materials. This, in turn, has spurred plans for new chemical plant investments in the U.S. across many products.

Billions in combined investments by companies are slated for projects—including ethylene, propylene and ammonia plants and crackers, with much of the activity planned to take place during the next four to five years. This bodes well for the pump industry from the standpoint of both greenfield and brownfield opportunities to drive business.

Europe

The European chemical industry is currently bleak, and the short-term forecast does not appear any more promising. The first half of 2013 witnessed negative growth in Germany and France, which are the largest economies in Europe. The demand from two key sectors—construction and automotive—is weak as those industries struggle through the general economic doldrums. Given the EU’s apparent rebound in the third quarter of this year, this industry is expected to witness growth of 1.5 percent in 2014 if general economic revival continues.

The pressure on the European chemical industry should not be overlooked because capacity is evolving back to the U.S. and continues to grow in Asia. Realizing that cost constraints could have a long-term effect on the region’s competitiveness on the global stage, the industry has turned to the concept of Verbund to build a sustainable path to compete. Simply put, Verbund is integrated to the maximum degree and rests on:

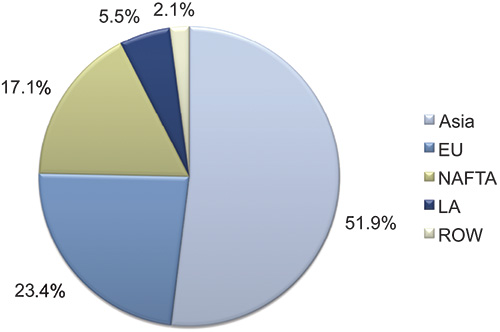

Figure 1. Global chemical sales

Figure 1. Global chemical sales- Production Verbund—integrated production

- Energy Verbund—minimization of emissions and effective use of byproducts

- Know-how Verbund—close global networking

- Supply chain Verbund—integrated logistics and supply chains

Companies have demonstrated dramatic process improvements and enhanced production metrics based on implementation of this process’ concepts.

China

China, the second largest economy in the world, is experiencing significant growth. The first half of 2013 saw somewhat slower growth based on both weaknesses in global demand and the effects of a domestic slowdown. The prospects for growth in China’s chemical industry are more dependent on government investment in the industry, rather than the demand for the chemical industry’s products (paints, adhesives, ceramics and various additives) because its economy is an investment-driven model.

The National Bureau of Statistics reported for the period ended on June 30, 2013, that investment growth remains more than 15 percent, despite that this activity may lead to overcapacity. Given the current scenario, growth in the sector through 2014 is still expected to be between 7 and 8 percent.

Pump Market Outlook

Economic volatility in 2013 has contributed to weak pump demand in this industry at a global level—the growth of the pump market during the first half of 2013 was basically flat. High growth areas, such as China, witnessed a drop in domestic investment because of a massive credit crunch.

North America and Europe witnessed low growth and negative growth respectively during the first half of 2013, but during the second half, conditions are expected to improve.

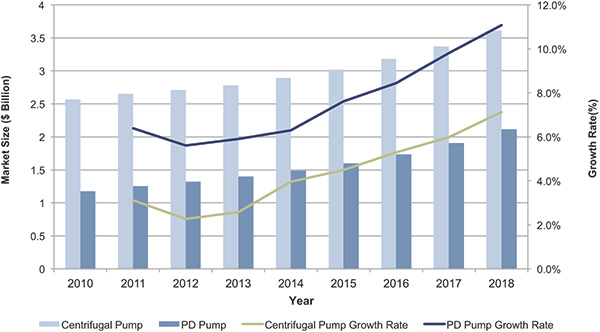

The growth of the chemical pump market contains much promise but rests heavily on general global economic strength. Investments in upgrades of chemical plants and the construction of new plants are expected to augment the growth of the pump market in the short- to mid-term. As shown in Figure 2, annual revenue growth is forecast to pick up post 2014. In the long-term, as more customers understand the advantages of positive displacement pumps in key chemical applications, positive displacement pump growth is expected to outpace centrifugal pump growth. Specifically, diaphragm pumps (because of their reliability and design for handling volatile fluids) and peristaltic pumps (used extensively because they are inexpensive and flexible in tubing design) are expected to experience continued growth in the space. The projected compound annual growth rate (CAGR) for centrifugal pumps is 4.9 percent, and the positive displacement pump market CAGR is expected to exceed 8 percent.

Figure 2. Global pump market overview—chemical industry

Figure 2. Global pump market overview—chemical industryConclusion

With a slowdown and flat growth witnessed in the first half of 2013 and questionable recovery in the second half, manufacturers are forced to maintain a low profile. Cost competitiveness in the U.S. and continued growth in China, however, promise pockets of opportunity in the industry. Merger and acquisition activities in the chemical industry and continued recovery in Europe could create additional momentum for short-term optimism, putting the pump market in this space on the path to stronger growth.